By Larry LaVercombe

This question rose again in my latest meeting with two prospective buyers: “When is the housing market going to calm down?”

“It seems like it’s been crazy for three years now. If we wait another year or two, will it be easier to buy? Will we be able to afford more, if we wait until we save more?”

My answer was that hidden within this question about “calming down” are two very different factors. There is the question about market speed and multiple offers, and there is also the question about prices and value. They were asking whether this was the right time to buy, or would it be easier/smarter to buy in a year or three?

Before I address this, I first want to make another point: Long term, the housing market is the single most dependable and cyclical market in the world. No matter what the interest rates, no matter what the political climate or how the economy is going, housing is directly related to the lifespan of the human being. People get married during wartime. People have children whether they have money or not. People die in good times. People get divorced... when they have to. Every one of these life milestones creates the need for different housing.

When I counsel my real estate clients, I often say that the Market Forces of the Moment will affect their sale in certain ways, and thus, from a financial perspective, there will always be good and bad times to buy or sell. But in most cases, each person’s personal life and personal timing will affect their course of action more than the specifics of any particular real estate climate.

Some people have the luxury of planning exactly when they will sell their home of 20 years. But most people are simply responding to their lives. Is this the right time for you?

“When is this housing market going to calm down? This is the calmest I’ve seen it since before COVID,” I said. The combination of Interest Rate Shell Shock with Minnesota Seasonality has made it so most realtors I know have nothing to do. We are like... hoping our one buyer buys... Or that our one listing sells.

So, if what you are looking for is a good time to go out and buy something when you have more than 24 hours to think about and you might even have negotiating power on price, then now is a great time. It’s calm.

If, on the other hand, you are asking, “When are the prices going to go down?” the answer is never. Not in Minneapolis proper. Never in the future will they be lower than now.

But if you are asking something a bit more nuanced, like: “If I wait two years, and I can save $30,000 during that time, will it be easier and better then for me to buy then? Or, will I have lost ground by waiting?”

I would say: “That’s the right question, and my opinion is that you would be losing ground.”

In my opinion, the advantages you would earn by having a larger down payment, and thus possibly a lower interest rate loan, would be more than offset by the increase in price of the home.

For instance: let’s say you want to spend $300,000 on your first house, and you have $20,000 saved for your down payment. You do have the $15,000 to purchase with a 5% down conventional mortgage, but if you saved $30,000 and then you had $50,000 to put down on a $300,000 house, that would almost enough for a 20% down payment... And isn’t 20% a lot better than 5%?

Yes – 20% allows you to avoid paying PMI, private mortgage insurance. But that insurance is much less expensive than it used to be, and the cost of PMI can be offset by your ability to invest 15% of your down payment elsewhere. And yes, in a competitive, multiple offer situation, the seller will often believe that a 20% buyer is better than a 5% buyer. (This belief is highly debatable, but it’s the norm.)

But more importantly: This $300,000 house doesn’t cost $300,000 anymore.

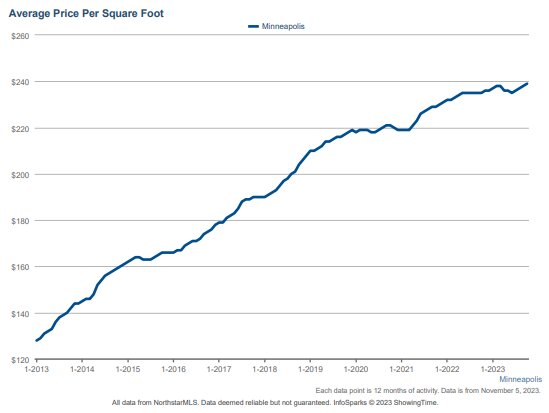

Minneapolis home prices have steadily risen a total of roughly 6.5% per year over the last 10 years.

If the annual appreciation is 5%, that $300,000 house will cost $331,000 two years from now.

Here is the point:

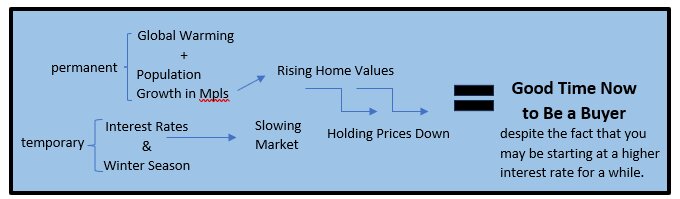

Since a) the market is dependably cyclical, and thus a year of quiet and calm will create a year’s worth of pent-up demand; and b) Prices are not going down in Minneapolis because a) our population is increasing, and b) people are moving here from highly-priced California because our climate is better, prices in Minneapolis are only going up. But they are right now being held down this month by the sticker shock of interest rates and the seasonality of the winter market in Minnesota.

ADVICE TO BUYERS

Find an agent that:

1. Can share their strategies regarding how they will advocate for you in a multiple offer.

2. Can help you make strategic decisions that will integrate your financial abilities with your individual life changes.

3. Doesn’t pressure you to act, but at the same prepares you for the distinct challenges of buying in this nuanced market.

In our Minnesota housing market, the sellers pay all the commissions. Sellers pay the buyer’s agent, and their own agent. So, if you’re a buyer, there is no reason not to find an agent to help you buy, and to find that agent well in advance of your being ready to put the trigger.

If you are educated in this market, you can win in this market.

Comments

No comments on this item Please log in to comment by clicking here